What is CIBIL?

What are the roles of the Credit Information Company?

What are the roles of the Credit Information Company?

What is Credit Check India?

Credit Check India is the country’s LEADING and PREMIER credit advisory company run by professional experts who have decades of experience and a long list of achievements. Our company aims to provide all the required assistance in helping the clients build good credit and boost their credit score for a better credit rating.

How can I get my CIBIL Credit Information Report (CIR) and TransUnion Score? You can apply online by visiting the CIBIL Transunion website and following these three steps. First, you will be asked to fill out an application form. Second, you will need to make an online payment in the amount of Rs.550. Lastly, you will be asked a few authentication questions to complete your application. You can check out the link below:

How soon can I get my CIBIL CIR and TransUnion Score?

If you have successfully answered the security questions, your CIR will be generated immediately and can be downloaded using your login username and password. If your authentication has failed, you will receive an email from CIBIL requesting that you provide an ID and proof of address (Utility bill, Certificate of Residency, etc.). Once completed, your report will be sent through mail.

What services do you offer? How can I enroll in the Credit Help India Program? We offer four service plans to fit your needs and budget. We have the Entry-Level Plan (for only Rs 999*) that offers to get your Credit Score. The Basic Plan (for only Rs 9999*) is an entry-level program that helps you understand your credit and provide you with the Credit Expert’s recommendations. The Standard Plan (for only Rs 12,999*) offers you a personalized Credit Expert who helps you build your credit. The Flagship Premium Plan (for only Rs 17,999*) offers to personalize the services. For more information, visit the Packages section.

How Does the Credit Score Change?

It is only natural for the credit score to fluctuate. Your credit report amends the details as reported to the credit bureaus. Banks and Lending companies report late payments of credit cards or EMI to the Credit Bureaus. The Credit Bureaus update it every month. During this time, the credit score can also change. You will see the three-digit number changes if the credit score is being tracked over time.

Your credit score is a snapshot of your credit behavior, and your credit report information is frequently updated. Based on your credit report, your credit score is determined. Lenders and collections companies update the information on your credit file. These data include balance adjustments, new accounts opened, payments to existing accounts, or closed accounts that fall off after the expiry of a term.

What is Considered a Good Credit Score?

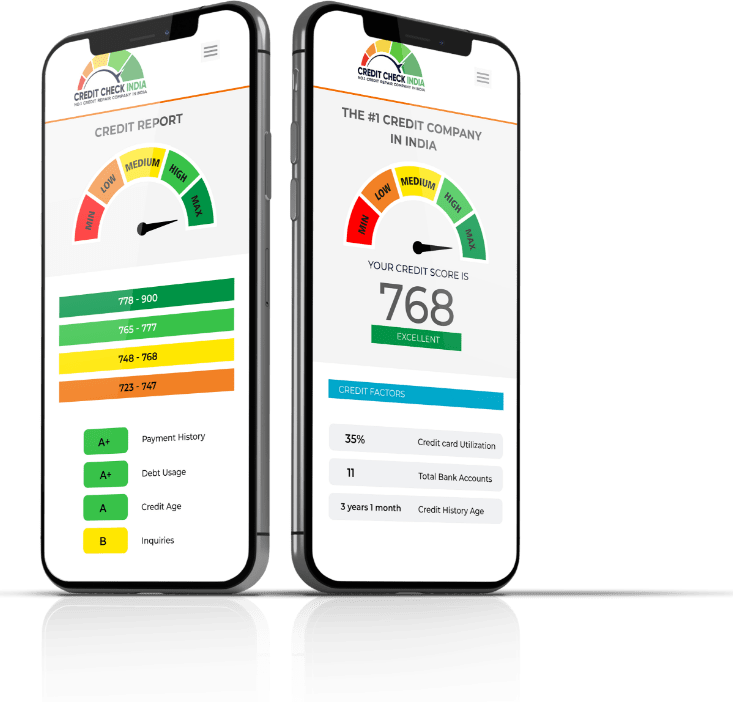

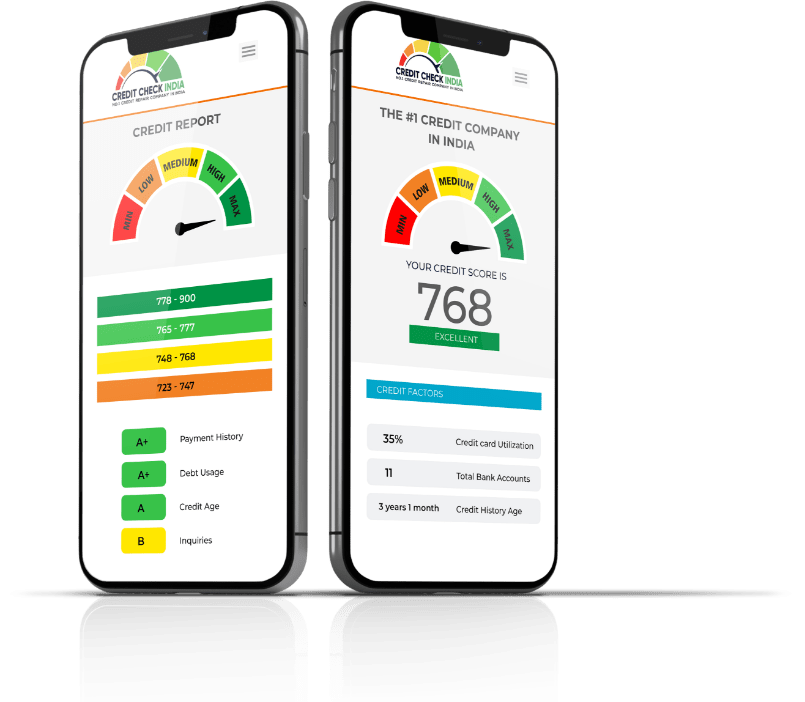

An excellent credit score is between 750 and 900. Banks, NBFCs, and other online lenders prefer such a loan score for candidates. You can be confident to be qualified for any credit product if you have such a credit score. It allows you to consider the range and the importance of the credit score.

no error noted on the table

The table shows that a loan score of 750 or higher is considered a positive score that could help you take advantage of many loan opportunities.

What Factors are Included in the Calculation of Credit Score?

Credit Bureaus (TransUnion CIBIL, Experian, CRIF High Mark, and Equifax) will consolidate your past credit history and repayment conduct. Usually, a credit score ranges from 300 to 900, with 900 as the highest possible score. The higher the score, the more creditworthiness is accredited to you and vice versa. A score of approximately 750 or higher is usually considered suitable for a lender like a bank to accept your application.

The following are the five factors that play a major role in calculating the credit score:

- Repayment History: The most positive influence on the credit score is the timely repayment of your existing credit cards. On the other hand, late repayments have negative effects on your credit score. The higher the percentage of your timely payment, the higher your credit score. This is one of the variables used to measure your score. A trustworthy borrower is noted by a clear timely payment pattern. Expect that the lenders are always optimistic that the debts will be paid on time. However, a late payment or two may have a significant negative effect on your loan score as it means that you cannot be counted upon to pay on time. It is a crucial factor in having a good score to pay all EMIs, credit cards, and other bills on time.

- Utilization of allocated credit limit: When you have 3 credit cards with a credit limit of Rs. 1 lakh each and you tend to almost repeatedly use the credit close to the limit, the risk would be high because the creditors might think that you are abusing your credit. On the other hand, your application for the 4th card will likely be denied if you do not use your 3 credit cards because the creditors might have the impression that you have excessively unused your credit limits. Therefore, it is safe to always use less than 30 % of the loan cap to best influence your credit score.

- The high percentage of unsecured credit: The best option for your portfolio is to provide a combination of secured credit (Home Loan, Car Loan) and unsecured credit (personal loan, credit card). It would have a positive effect on your credit scoring. A combination of various types of loans to show fast reimbursement would have a positive effect on your ranking. If your portfolio includes a high percentage of unsecured loans, your credit score would be negatively affected.

- Length of credit history: Having a longer credit history is better because the creditor could assess and have more accurate knowledge about your credit behavior. If you hold a credit card for three years, for instance, future borrowers could see a substantial amount of time for the repayment behavior on the card. Your bank might become skeptical if they don’t know enough about your payment habits. It is also advisable that you don’t close your old credit cards as they offer prospective lenders a more complete credit image.

- Excessive loan applications: The lender will receive a copy of your credit report when you apply for a new loan to decide whether you are eligible or not. This is regarded as a credit investigation. Too many credit inquiries might hurt your credit score without a corresponding approved loan. If you notice a lender has declined your request for a fresh credit, other lenders are most likely to decline your request for the loan. Even if they accept your loan application, there might be too many requests that might have a harmful effect on your score within a short period.

- The number of negative markings: Listings like write-offs, settlement, DPD, suits filed against you are negative flags in your credit report. Having a couple of these listings could be a crucial factor that might significantly limit your eligibility for a loan. A negative listing demonstrates that you have not handled your credit properly and serves as a warning to future lenders.

Will The Credit Score Be Affected For Owning Multiple Credit Cards?

Credit is extremely important in accomplishing your goals and the emergencies triggered by various causes. A decent credit score is crucial if you want to achieve the right loan. A credit Score also applies to your credit behavior.

Your credit-related behavior affects your credit score. It begins immediately with your credit application and continues with each refund until the credit instrument is closed. Both acts affect your credit score either positively or negatively, depending on your credit behavior.

Borrowings, along with credit cards, overdrafts, credit limits, etc., are an essential form of credit. It is therefore incorrect to show that loans would harm your credit. Remember that you wouldn’t get a credit score without any credit. It could be difficult to receive credit like a chicken and egg scenario without a credit score. But at the end of the day, a vast range of options are open to those who choose to use credit but have no credit history. However, there might be some circumstances in which the credit effect may be negative.

Determinants of Your Credit Score

A credit score will be assigned according to several variables. It is important to know the different factors that determine your credit score before knowing how loans affect your credit.

- Your Credit Accounts: The number of loans and credit card accounts whether those are positive or negative accounts.

- Repayments on your Credit Accounts: Punctual repayments on your credit accounts are one of the main components of a credit score.

- Credit Mix: A good balance of secured and unsecured accounts is a foundation of a good credit score.

- Credit Mix: A good balance of secured and unsecured accounts is a foundation of a good credit score.

- Credit History: A strong and long loan relationship works a lot for your loan worth. Many clients who are new to loaning would have to build it up.

- Credit Utilization Ratio: Using your credit card wisely is very important. You have to be careful not to reach the specified limit of 30-40% in your utilization ratio. This will show that you are not an abusive debtor.

- Number of Hard inquiries: Each credit application is considered a hard inquiry. The higher the number of your hard inquiries in a short period, the lower your score would go.

What Can I See in My Credit Report?

You can find all your account information, requests, and public records. In all your credit reports, you will also find the following:

Personal information

- Complete name and other names, such as maiden and bachelor’s names, nicknames, and middle names you might have used in previous loan applications.

- Birthdate

- Current and prior addresses associated with your credit accounts.

- Phone numbers that are associated with your credit accounts.

Accounts

- Current and historical credit accounts from the past, including revolving (Credit Cards) and installment accounts (mortgages and loans).

- Name of the creditor/lender.

- Opening date/closure.?

- Status (current or past due)

- Credit limit (for credit cards) or loan amount.

- Balances, such as the current and the highest.

- Payment history.

Inquiries

- Banks and Lending Institutions that have pulled your credit report.

- Your report was being accessed.

Is It Possible To Delete the Information From The Credit Report?

A significant part of your financial journey is your credit report. This is vital because we all find that at one point in our lives, we need credit. It may be for purchasing an asset such as a home or a car, financing education, coping with crises such as medical emergencies, financing a marriage, a vacation, or simply surviving every day.

No matter what your needs might be, this form of need is credited. What you need to apply for credit though is a decent credit score. Not only is credit responsible, but it also keeps your credit report clean.

A Clean Credit Report

What does a clean report have to do with credit? The report is error-free, and any feedback will harm your credit health and end up impacting your chances of earning credit the next time you need a credit card or loan.

Six basic steps to help you clean up your credit report:

Get a copy of your Credit Report: You can get it for FREE on CREDITCHECKINDIA.COMVerify the information: Check if the information in the report are all correct.

Get rid of the errors: If you encounter any error, report it immediately to the credit bureaus.

Evaluate the number of your credit accounts: If you have many accounts, it’s time to free up some accounts and improve your debt-to-income ratio.

Resolve negative accounts: Negative accounts reduce your credit score. Resolve these accounts at the earliest with the help of Credit Check India.

Improve credit score: Improve credit score to get the best loans and credit cards.

Step 1: Obtain A Copy of Your Credit Report

You should review your report to be able to update your loan report. It is best to either reach out to a competent credit management service like Credit Check India to help you understand your credit report and get advice on how to clean up your credit report and boost your credit score. Most clients are not familiar with the credit report and how it affects our lives. It is high time that you get a copy of your credit report if you are thinking of applying for a loan. Knowing your loan report and its elements will allow you to address your credit report issues more quickly if there is any.

Step 2: Verify the Information in The Report

Your credit score is assigned based on the details concerning your credit conduct, which your lenders submit to the Credit Bureaus. It provides information on all your credit accounts, whether open or closed, your repayment history: whether it has been replaced or is not repaid promptly, your credit use ratio, your credit mix, your credit history, and your PAN’s extreme request. It includes all your credit accounts, whether open or closed. The information in your credit report is very important to review to maintain the accuracy of your credit data.

Step 3: Get Rid of The Errors in The Report

Unforeseen errors in your credit report may cause inaccuracy and may not be considered as valid. Inaccurate information in your credit report might have a negative effect on your score. Your credit report must be checked as much as possible to decide if any mistakes exist in your report. The errors can be corrected through a simple dispute resolution procedure.

The most commonly found errors in a Credit Report are:

- Error Type

- What it means

- Effect

Identity Issues

- Incorrect PAN or personal information

- Medium-High

Account Errors

Wrong reporting of credit limit, loan balances, account status High.

Identity theft

Someone else uses your identity and conducts fraudulent transactions under your name

- The PAN is the basis for a credit score. PAN numbers or names can be mixed with those of another person with similar documents due to surveillance or clerical error.

- Such mistakes which show an incorrect credit cap, incorrect loan account balances, closed loans as Settled or Write-offs, or the same loan more than once.

- Credit report errors can also be attributed to identity fraud, in which a person uses another person’s identity to receive credit. These are more serious and should be reported to the Police.

Step #4: Evaluate the Number of Credit Accounts You Have

A clean credit report shows your creditworthiness and is free from errors. You should focus on the number of your credit accounts while you finish sorting the errors in your credit report.

It might be the time for you to review the situation and try to close some if you have multiple credit accounts such as loans and credit cards. You will find it hard to get new loans if you pay EMIs above or near a specified cap of 30% of your gross income. It is good in such cases to plan a budget to pay such loans in advance, so that a portion of your revenues is issued.

Step #5: Work on Getting Negative Information Off Your Report

Negative details such as settlement, written off, suits filed, etc. could be due to your earlier delay or default on repayment of loans and credit cards. A loan report with negative details is converted into a low loan score that can affect your future loan prospects. It is therefore good to get your credit report off the negative details at an early point. Your report on a representation or submission from your end cannot just be deleted. However, experts warn you that you will stay on your credit report when it comes to significant negative data such as payments or defaults.

Step #6: Start Working Towards Building a Good Credit Score

There will always be a need for credit. It cannot be achieved immediately to build a good credit score. It needs continuing attempts to be liable for a longer period. It could take three months for some people, and it might take up to a year for others, depending on the size of the report and the amount of negative information you receive. As the credit score and credit report have recently grown significantly, it is impossible to be laid-back and have a good score and report.

Who Can Access My Credit Report?

A variety of entities and third parties can access your Credit Ratings and Credit Reports. Some of the organizations and individuals that can draw your reports or a ranking are:

- Banks: When you apply for a loan or a credit card, the bank will pull up your credit report to verify your creditworthiness. If you opt for an overdraft facility, your credit will also be pulled, and this is known as a credit line.

- Creditors: Present or prospective creditors — such as issuers of credit cards, auto loans, and credit lenders — may draw the credit report to assess your creditworthiness. Credit history is an important factor in the assessment whether a loan or credit card is to be issued. The higher your credit, the more likely it is that a loan with positive interest rates would be accepted.

- Employers: Employers like banks, NBFCs, and some IT companies have started checking the credit report of employees before offering a job. It is very critical that you keep your credit health and credit report in check and in good shape so that your job application is not rejected based on bad credit history.

What Credit Score Do You Need to Get Approved for a Credit Card?

A card with a score of less than 750 may be accepted, but you may be subjected to less favorable conditions such as a card with lower limit and annual charges or fee. The lower your Credit Score, the higher your risk of dismissal. It would be very difficult to accept a credit card application if you have a score of less than 650. Another disadvantage of applying for a low score credit card is that it causes your score to go down every time your application is denied. When you have a low credit score, applying for a credit card means facing repeated rejections and a gradual decline in your credit score. It is a good idea to review your credit score and plan on how to increase it, and make sure that your application is accepted first before applying for another credit card.

How Can I Improve My Credit Score?

Here are some quick tips that will help you improve your credit score quickly:

- Pay all your EMIS (Education Management Information System) and credit card bills on time. Remember, your repayment history is up to 30% of your credit value. It is important that you ensure that you have a perfect repayment record from past to present. Making complete payments on time would affect your credit value instantly.

- Get a copy of your credit report and look for errors to have them resolved as soon as possible. A loan which you have paid in full can still be marked as unpaid due to reporting errors by banks and lending companies. These errors will pull down your Credit Score unnecessarily. If you challenge and correct these errors, your score will get automatically positive. A wrong detail or misinformation may also harm your Credit Score. It is also important to look for incorrect entries that may also suggest identity theft. Solving these glitches will increase your Credit Score.

- Try your best to spend less than 30% of your credit card limit. If your credit card limit is Rs 1 lakh, make sure that you don’t spend more than Rs. 30,000 on your monthly purchase. Maintaining your credit limit constantly within 30% will automatically increase your ranking.

- Do not make several applications within a limited period for loans or credit cards. Clients often think that applying to several lenders for several items (Home Loan, Car Loan, Credit Card or Personal Loan), they can increase their chances of obtaining a loan. Remember, potential lenders may run an inquiry every time you apply for a new loan. Too many inquiries will lead to a decrease in your credit score and may give you a negative image.

- If you have a low Credit Score, DO NOT apply for a new credit (whether a Loan or Credit Card). Any loan refusal has negative consequences on your Credit Score. Make sure that your creditworthiness is good before applying for a new loan. This will avoid loan refusals and successive decrease in the ranking.

Can I Have More Than One Credit Report?

A comprehensive report can be downloaded once a year from the Credit Bureaus free of charge through electronic form.

A credit information report (CIR) describes a credit information company’s credit history. There are four Credit Bureaus (CIC): TransUnion CIBIL, Equifax Credit Information Services, Experian Services India, and Highmark CRIF.

The lender asks credit bureaus for your credit report every time you apply for a loan. The details in your credit report indicate how you treat your credit and your monthly payments.

A score of 300–900 is assigned based on this information. The score for the same person with a different bureau varies to a certain degree but not dramatically because the underlying data are generally equal. The score changes may be due to the weight provided by lenders and their algorithms for various categories of knowledge.

Generally, you purchase your credit report online. You have to provide information such as date of birth, PAN, and email address. However, you can obtain a copy of your credit report from each credit bureau free of charge once a year. You can get your credit report through the Credit Bureau’s website.

Why should I enroll in the Credit Check India Program?

Are you facing the problem of getting a loan or Credit card? Are you facing job rejection? Do you want to know and understand your Credit Report? Does your Credit Score is less than 750? Does your Credit report reflect an error? Does your Credit report reflect Settled, Written, or Post written off Settled remarks? Are you paying a higher rate of interest on Loans? If you have any of these problems, then Credit Check India is the ultimate solution! Our Personalized Credit Expert will help you understand, build, and boost your credit to a healthy level. For more inquiries, please write to us at care@credithelpindia.com

https://credithelpindia.com/get-credit-report

Curious About Your Credit Score? Get Your Credit Report for FREE!

Fill Out the Form Below:

Before You Start, Here’s Everything You Need to Know.

If you want to know more about your financial situation, you should get a free credit report online. Your Credit Score will determine whether or not you can acquire loans, credit cards, or other forms of credit. It will also affect the interest rates and terms of those loans. Below you will find some tips for obtaining your free report. These will help you learn about your Credit Health and Credit Score. Although it is not necessary to check your Credit Score, it is still best to do so regularly.

What does Credit Report Include?

A free credit report will include detailed information about your finances. Usually, it contains the credit history of your payments on your past and current accounts. It also shows the credit limit that you have used. Some of the information in your report may not be accurate or up to date. Fortunately, you can obtain a free copy of your credit report through Credit Check India. Always read and review your credit report to ensure that all information is correct,

Does My Credit Report Show My Actual Credit Score?

First, you should learn what your credit report contains. It shows your Credit Score and tells you about your credit history and health. It includes all of your payments and account balances for all types of loans. If you have a poor score, you’ll notice some accounts with late payments reported to collections due to default. You can use your free credit report to improve your Credit Score.

If you are looking for solutions to improve your credit score, do not hesitate to reach out to us! We provide the best solutions to all your problems and guarantee an increase in your Credit Score!

CIBIL Commercial Report & CIBIL Rank

CIBIL Commercial Report is a report card of MSMEs of credit history and behavior. CMR (CIBIL MSMS Rating) is a ranking between 1 and 10, with 1 being the highest and 10 being the worst. CIBIL Commercial Credit Report( CCR) is prepared by Transunion CIBIL. Commercial Credit Report is highly usable and actionable that provides a detailed insight into a business entity to whom Bank is lending.

List of topics covered:

- What Is CIBIL Commercial Report

- CIBIL Score vs CIBIL Rank

- How To Read CIBIL Commercial Report

- Importance Of CIBIL Commercial Report

- List Of Documents Required For CIBIL Commercial Report

- Factors Affecting CIBIL Commercial Report

- FAQs

What are CIBIL Commercial Report and CIBIL Rank?

CIBIL Commercial Report

Even though a CIBIL score refers to the lending value, a trade report by CIBIL underlines the lending worth of a company. CIBIL commercial report is a systematic declaration that shows the financial health of the company in terms of information obtained from the bank and other financial institutions. This detailed report is for the creditworthiness assessment when a commercial loan is needed.

The following information are included in a CIBIL commercial report:

- Company background: Includes background information on the company such as the legal establishment, branches, ownership, and operating years.

- Financial information: Financial data that decide the company’s credit standards.

- Financial history: Finance info, including payments, collections, income production, and more relevant to the financial history of the company. Other than these, the CIBIL rank is also essential. A rank of CIBIL resembles a score of CIBIL. It numerically summarizes the company’s CCR. Just like the score of CIBIL is between 300 and 900, a CCR ranges from 1 to 10, where 1 is the best possible. Only businesses with Rs.10 lakh credit exposure to Rs.10 crore are granted this designation. You have a higher chance for a business loan to be secured if you get closer to 1.

CIBIL Rank

CIBIL Rank is equivalent to the CIBIL score given to individuals, provided to commercial organizations. It sums up the complete Company Credit Report (CCR) on a scale of 1 to 10 in one digit. The credit rank shows the chance of default payments. Therefore, the lower the ranking, the more likely the loan is. Therefore, 1 is the highest possible ranking. Remember, however, that a credit rank is not allocated to all firms. The credit rank applies to only companies with loan exposure of 10 lakh to 50 crores.

CIBIL Score vs CIBIL Rank

Companies also apply for loans to run and expand their business and in the process of loan approval banks and lenders generate Commercial Credit Reports from Transunion CIBIL and other Credit Bureaus to check the creditworthiness of a borrower.

Below is the comparison and the difference between individual CIBIL Score and CIBIL Rank for you to have a better understanding of both. Individual CIBIL Score has a three-digit figure between 300 and 900. CIBIL Score more or equal to 750 means greater chances of loan approval. Summary of past and present loan track record for the company and firm ranking ranges between 1 to 10, 1 is the best and 10 is the worst.

How to read CIBIL Commercial CIBIL?

Commercial Credit Information Report contains detailed information about a business entity which may be Proprietorship, Partnership, LLP., Private Ltd, or a Public limited firm.

Following are the different sections covered in a Commercial Credit Report:

- Identification: It is present at the top and contains the Report Order Number, which indicates the number of times your report has been accessed from CIBIL’s database.

- Inquiry Information: This section specifies the name of the company, an identification code, and address.

- Borrower Profile: It is further divided into 4 sub-sections:

- Borrower Details: It includes company name, legal constitution, class of activity, etc.

- Address and Contact Details: It includes the registered office address, phone number, etc.

- Identification Details: It includes the company’s PAN, company registration number, etc.

- Delinquencies Reported on the Borrower: It includes the payment status of the company and the guarantors.

- CIBIL Rank: This section displays your credit rank, which ranges on a scale of 1 to 10. The lower the rank, the better are the chances of getting a loan.

- Inquiry Summary: This section displays the list of inquiries done by lenders in the recent past.

- Derogatory Information: This section contains information regarding defaults, and overdue and dishonored cheques.

- Outstanding Balance Details: This section provides an overview of the company’s asset classification concerning the credit facilities availed.

- Location Details: This section mentions additional contact information of the company.

- Related Parties Details: It gives information about the related individuals or entities.

- Credit Facility Details – As Borrower: This section contains details of the credit facilities availed by the company. It contains credit facility details, payment status, and overdue details.

- Credit Facility Details – As Guarantor: This section contains details about the credit facilities guaranteed by the company.

- Suit Filed Details: It gives details of suits filed (if any) by any of the previous lenders for the company.

- Credit Rating Summary: It contains the latest three credit ratings assigned to the company by an external accredited rating agency.

- Inquiry Details (Last 24 Months): This section provides details regarding the inquiries made by lenders for your company’s credit application.

Importance of CIBIL Commercial Report

CIBIL Commercial Report is a very important document when a company approaches Bank or lender for a loan or credit facility. This report shows the behavior and financial discipline of lenders and proves the creditworthiness of a borrower. CIBIL Rank gives an idea about the riskiness of a borrower and helps the lender in deciding on approval or rejection of loan approval. CIBIL Rank of close to 1 increases the chance of loan approval. A good ranking is a key indicator that how likely the prospective borrower is to repay the loan on time and without default.

Documents Required to Check CIBIL Commercial Report

For Public and Private Limited Companies

- Proof of Address (any 1): Electricity or telephone bill, bank account statement or passbook, registered lease/ sale agreement of office premises, address proof issued by commercial or multinational banks, registration certificate issued under Shops & Establishment Act.

- A copy of board resolution along with authorized signatory list and specimen signature.

- Company PAN.

- Proof of Identity of one of the authorized signatories: PAN/ Passport/ Driving Licence.

( Any utility bill or telephone bill should not more than ninety days old )

For Partnerships

- Proof of Address (any 1): Electricity or telephone bill, registered lease or sale agreement, bank account statement, etc.

- Copy of partnership deed or certificate of registration.

- List of authorized signatories with specimen signatures.

- PAN of the partnership firm.

- Proof of Identity of Partner requesting the Company Credit Report: PAN, Driving Licence, or Passport.

- For Proprietorships

- Proof of Address (any 1): Electricity bill, registration certificate issued under Shops & Establishment Act, etc.

- Proof of Identity of the Proprietor: PAN, Passport, or Driving License.

- NOTE: The above documents should be self-attested by the proprietor. Any utility or telephone bill should not be more than ninety days old.

Factors Affecting CIBIL Commercial Report

Following is the list of the major factors which are taken into consideration while preparing the CIBIL Commercial Credit Report (CCR), and the CIBIL Rank:

Payment History: This refers to the financial discipline of the company while making repayment to the lender. Timely making loan repayment and interest servicing of overdraft/cash credit help in having a good CIBIL Rank.

Credit Utilization Ratio: This refers to the ratio of credit used by the company out of the total credit (loans and overdraft) available to the company A high credit utilization ratio shows the company as credit dependent on external funds to run the business hungry, instead of internal cash flow and thus negatively impacts the Company Credit Report and CIBIL Rank.

Length of Credit History: It refers to the duration over which the company has availed loans and repaid them. A longer credit history generally translates to a good CIBIL rank, provided the payments were made punctually.

Outstanding Debts: This refers to the sum of ongoing loans and other outstanding debts of the company which a company is supposed to repay. A large amount of such overdue or outstanding indicates lower repayment ability and a highly leveraged company and lower the CIBIL Rank.

Vintage and Size of Company: Companies that are in their current business for a long period have better chances of loan approval since vintage companies are perceived as more creditworthy and have a high rate of loan approval and also avail of loans at a low rate of interest with easy terms and conditions. Stability and continuous growth help lenders in taking quick decisions.

Turnover and Profit of Business: The turnover of a company tells about the size of the company and the profit of the company shows how efficiently and professionally a company is being run by its owners. High turnover and good Profit have a direct bearing on repaying capacity of a company. Generally higher ratio of profits and turnover facilitates a firm to avail of loans to meet their credit requirement.

How can I Improve my CIBIL Rank?

The following are some key actions that can help you improve the CIBIL Rank as these get recorded in your commercial CIBIL report:

- Always pay the loan EMIs and other outstanding dues on time to maintain a good repayment history.

- Try to maintain a low credit utilization ratio to improve the company’s creditworthiness.

- Sustain a long and good credit history to improve your company’s credibility.

- Always maintain a feasible amount of outstanding debts, so that the company’s repayment ability is not affected.

- Maintain a good balance between the company’s assets and available liabilities.